Panic washes over me. The realization that I’m broke, penniless and destitute sinks in. How will I provide for myself? My family? Where will I live? I wake up in a cold sweat, heart pounding, pulse thumping in my ears. Slowly, I return to wakefulness and I realize I was only having a nightmare.

But what if it really happened? What if I woke up one day and realized my investment portfolio was depleted and I couldn’t feed my family?

Spending all the money in my investment accounts would definitely qualify as an “early retirement failure”. This kind of failure is what some early retirement naysayers claim will happen if you quit working before age 65. But is it really possible to suffer this kind of catastrophic early retirement failure?

I don’t think so. Here are five reasons why:

1. We only spend a tiny fraction of our total investment portfolio each year.

The standard rule of thumb for retirement spending is that you can spend 3% to 4% of your investments each year. Flip this rule on its head and you see why I’m not too worried about spending it all. Every year early retirees don’t spend 96% to 97% of their investment portfolios.

Put another way, since we spend only 3% of our portfolio each year, it would take us 33 years to deplete our portfolio (assuming zero investment returns for all 33 years). We have a 33 YEAR emergency fund at our disposal.

What if the unthinkable happens and our investments get cut in half overnight? We still have adequate assets to last for 16 more years! I don’t think we could live forever on a portfolio balance half its current size, but we will have plenty of time to adjust course and figure out our next steps. We could wait and see what happens with the markets for a year or two, or wave the white flag and head back to work as soon as possible.

2. Dividends and Interest.

Part of our annual expenses are funded by dividends and interest. Dividends can fluctuate year to year but are relatively stable. Interest payments are very stable. Our portfolio yields around 2.2% to 2.4% each year, which is just a little bit less than our annual spending. We don’t really need big returns in the stock market to fund our annual expenses, as dividends and interest cover most of our annual spending. In our taxable accounts alone, I expect around $8,000 per year in dividends and interest, which is enough to pay 25% of our $32,000 budgeted retirement expenses and enough to pay 33% of our “core” expenses of $24,000 per year.

3. Availability of other income sources

The core foundation of our early retirement financial plan is an adequately sized investment portfolio. But it’s not the only source of income available to early retirees. If we saw our investment balances dropping quickly, we could supplement our portfolio withdrawals with other sources of income. Part time temporary jobs, self employment income, profits from hobbies, selling your stuff on ebay or craigslist, or doing odd jobs can all provide additional income streams while the investment portfolio continues to do the heavy financial lifting.

I suppose some would demand the forfeiture of your honorary early retiree badge if you were to accept the idea of “doing work in exchange for money” as a valid pursuit during retirement. That’s a very binary view of life. I’m okay with others placing themselves within artificial constraints. Lucky for me and everyone else on the planet, we get to make our own rules in life. Like how we define “retired”. It can be pretty easy to earn money with a part time pursuit that you enjoy, just be sensitive when using the word “retired” around those that would seek revocation of your early retiree badge.

In a guest post here at Root of Good, Nick from Pretired.org laid out a case for rethinking retirement altogether. That article might help frame your conceptual take on early retirement and the role of making money even though you are “retired”.

4. Flexibility With Annual Spending

Even though our retirement budget is $32,000 per year, we don’t have to spend $32,000 every year. I intentionally added some wiggle room into our budget so that we could shrink our spending in years when our investments struggle to hold their value. Vacations, gifts, entertainment, and dining out represent over 25% of our annual budget. We could trim a few thousand dollars from these categories and still live a perfectly wonderful life.

5. Social Security

We are still three decades away from Social Security. Under the current SS rules, we will be entitled to payments that can fund two thirds of our retirement budget. Maybe Social Security will still exist when we become eligible, or maybe SS will be modified to our detriment. I’m guessing it will still exist in some form. I haven’t explicitly factored SS into our retirement budget, but knowing that there’s a good likelihood of receiving something 30 years from now provides an extra layer of financial security.

Minimizing Risk Of Early Retirement Failure

During our early retirement, we rely on our investment portfolio to generate our living expenses. We also expect the investment portfolio to grow over time to keep up with inflation (at a minimum). Even though we have a big fat investment portfolio, it doesn’t mean we can rest on our laurels and ignore our finances.

Here are some tricks anyone can use to keep early retirement finances on track:

1. Track spending.

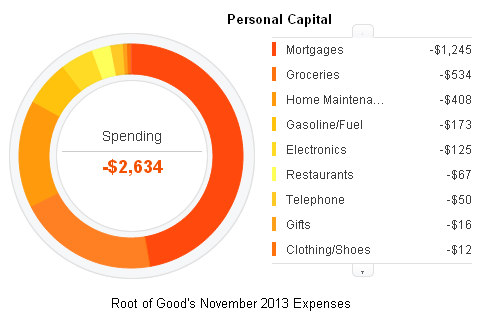

Are your expenses trending up or down? Are some categories growing disproportionately? Do we need to trim expenses to keep within our budget? The easiest way to automate expense tracking is with Personal Capital (review of Personal Capital). Personal Capital does all the heavy lifting by automatically consolidating your purchases and bill payments from your credit cards, debit cards, and checking or savings accounts so you have a full view of your spending all in one place. Automatically. For free. You can’t beat the price and level of effort required to get a complete view of all spending.

2. Manage investments.

In general, you don’t want to look at your investments on a daily basis. The fluctuations will drive you insane and force you to make emotional (dumb) decisions. Keep your eyes away from your investments and your hands off the “buy” and “sell” button at your brokerage firm. Go out, live life, and have fun instead.

You do need to keep track of your investments and make sure you aren’t going broke. Monthly or quarterly check-ups will do the job. It’s infrequent enough that you won’t suffer much emotional pain if the portfolio value dips. The last thing you want to do is sell when your investments are down. Remember the “buy low, sell high” rule to getting rich in the stock market? Don’t do the opposite.

In addition to tracking expenses, I also use Personal Capital to gather all my brokerage accounts, 401k, 457, IRA, and HSA holdings into one screen so I can quickly determine my total investment portfolio balance. I love spreadsheets and have a number of them to do more detailed analysis, but I pull data from Personal Capital to populate my other investment management spreadsheets.

If you notice your portfolio has dropped 20%, don’t panic, but pay attention. Your investments will most likely recover over the next couple of years. But it may be time to consider a plan B to get some supplemental income flowing in order to take some pressure off your investment portfolio.

As part of your investment management, don’t forget to rebalance your portfolio. Here’s how I do it. While you are rebalancing, keep in mind tax implications from selling appreciated assets. As you are rebalancing your investments, you can also sell appreciated assets to generate cash to fund the next quarter’s budgeted expenses.

3. Generate more income.

I already touched on the possibility of other income streams. If you have adequately saved and prepared for early retirement, you don’t have to focus too much energy on earning even more money. Just be aware that the option to earn a buck is out there if your portfolio starts to get rough around the edges. Think about your hobbies or interests and how you can make some cash doing what you love.

Getting some cash flow coming in the door can also help relieve the psychological fears of running out of money due to exhausting your investment portfolio. In our situation, we plan on spending $32,000 per year which is around 3% of our investment portfolio. If Mrs. Rootofgood and I make just $8,000 per year from part time pursuits, hobbies, or odd jobs, we will have enough to fund 25% of our annual spending, and bring our withdrawal rate closer to 2%.

$8,000 per year isn’t a big number. It equates to $333 per person per month. I happen to make more than that from Root of Good right now, but I could also make that much doing a ton of different things that are interesting or challenging (in limited quantities). Fixing appliances, light handyman/construction tasks, yard work, dog walking, babysitting, tutoring, running errands, participating in focus groups, or ebay/craigslist selling could easily net $10-25 per hour. To earn $333/month at that rate of pay, you would have to work 3 to 8 hours per week. Not exactly hard work. Maybe you don’t like doing any of those jobs I mentioned, but I bet you are sufficiently creative to come up with a few things you wouldn’t mind doing a few hours per week.

The concept of working during retirement may not be to your liking. That’s okay, because you probably won’t need to work another minute if you don’t want to (assuming you’re only spending 3-4% of your investments each year). The odds are strongly in your favor that your portfolio will rise enough over your lifetime that you’ll be just fine. But if you are genuinely scared of running out of money when there’s a dip in the stock market, earning a little supplemental income is a great way to put your mind at ease and take a little stress off your hard working portfolio.

4. Adjust spending in hard times.

Getting in some supplemental income is great, but you can also keep your early retirement on track by trimming expenses when your portfolio takes a hit. You’re already following tip #1 “Track Spending” and you have Personal Capital quietly capturing all your expenditures, right?

Find areas where you can cut back temporarily. Skip the long overseas vacation this year and explore local tourist destinations in your own state or within driving distance. Skip the luxury hotel and find a good lower tier hotel that has solid reviews. Travel off season.

An even better way to cut vacation expenses is to figure out travel hacking. Sign up for some credit cards and snag some free flights and hotel stays. And get some cash back bonuses from credit cards. We flew half way across the world to Argentina and Uruguay for free using frequent flyer miles from credit card sign up bonuses. Once we arrived, we enjoyed the region’s low costs on restaurants, entertainment, local transportation, and hotels.

When you’re at home, skip some expensive restaurants and work on improving your cooking skills. You can often replicate expensive entrees at home for a fraction of the price, and tweak the salt, oil, and butter to your tastes to make the dish a bit healthier. And you save money.

There are also big expenses that can be postponed for a year or two if your investment portfolio is temporarily depressed. Major home maintenance, replacing a car, and optional medical or dental procedures all fall into this category. Eventually these big lumpy expenses will be a necessity, but there’s usually some flexibility with the timing.

Failing Early Retirement Due to Boredom

I haven’t seen any academic papers on the topic of “early retirement failure”, but I bet a common cause of returning to work isn’t financial, but rather mental. Some people aren’t cut out to provide their own entertainment all day. Think of prisoners serving a life sentence. After decades of incarceration the inmates would have an extremely hard time adjusting to life outside the walls of their cell.

Maybe the office cubicle is the perfect environment for those who can’t handle the freedom of choosing what to do all day. But that’s another topic for another day. I’ll have to address the non-financial aspects of early retirement failure in a future post.

Don’t Fear Early Retirement

In this article I have explained why the risks of running out of money aren’t as dire as some fear. We are humans, not mindless machines stuck in an endless loop of unbridled spending without any feedback from our own finances. If an early retiree’s investment portfolio hits a speed bump, that retiree has a number of options before declaring their early retirement a complete failure and heading back to work full time out of financial necessity. As outlined in the tips above, the early retiree would be wise to keep track of expenses and investments, and be ready to earn some supplemental income or trim expenses when their investment portfolio starts to wilt.

Do you fear running out of money during early retirement?

Root of Good Recommends:

- Personal Capital* - It's the best FREE way to track your spending, income, and entire investment portfolio all in one place. Did I mention it's FREE?

- Interactive Brokers $1,000 bonus* - Get a $1,000 bonus when you transfer $100,000 to Interactive Brokers zero fee brokerage account. For transfers under $100,000 get 1% bonus on whatever you transfer

- $750+ bonus with a new business credit card from Chase* - We score $10,000 worth of free travel every year from credit card sign up bonuses. Get your free travel, too.

- Use a shopping portal like Ebates* and save more on everything you buy online. Get a $10 bonus* when you sign up now.

- Google Fi* - Use the link and save $20 on unlimited calls and texts for US cell service plus 200+ countries of free international coverage. Only $20 per month plus $10 per GB data.

“Put another way, since we spend only 3% of our portfolio each year, it would take us 33 years to deplete our portfolio (assuming zero investment returns for all 33 years). We have a 33 YEAR emergency fund at our disposal.”

Doesn’t this assume zero inflation over 33 years?

Coincidentally, I just ran across my monthly budget from 35 years ago. I spent $212 per month. Today that’s about what I pay monthly for telecom alone.

I guess I should have clarified zero investment returns as “zero REAL investment returns”. Good catch though!

At 3% inflation, and zero nominal returns, our nest egg would still last 23 years. In other words, plenty of time to realize we had a problem with our investments and we had to do something to earn more or spend less. Interestingly, in the 23rd year, we would have to spend $61,000 to buy the same things we buy today for $32,000 (or almost double!). Inflation is the real killer for early retirees.

And wow at only spending $212 per month back in 1978! According to the CPI-U, costs have increased by 246% since then. That means you only spent $733 per month (in 2013 dollars) back in 1978. That’s way less than we are spending today, for sure! And I imagine you have experienced lifestyle inflation that led to you spending more than $733 today (if you are spending $200 on telecomms alone today). In fact, telecom for most people in 1978 was a single telephone. No cells, no internet, no cable tv in some places.

Great post, Justin!

I think that retiring in our 30s-50s gives us even more opportunities to succeed than in our 60s. The multi-decade head start gives us the confidence that our portfolio will survive, and the skills to enjoy redesigning our lives.

After 11 years of retirement, I still wake up in an occasional cold sweat after dreaming that the Navy needed me back for “just one more tour”…

Who knows, you might get that call one morning. “Doug, the President needs you. Shave off the pony tail and get down to the dock by 0800.” Or at least that’s how it would happen in the movies.

As for running out of money, I would rather figure out I was running out of money in my 30’s or 40’s than later on. I figure I have a better chance of finding gainful employment at a younger age.

Yeah, technically that’s what it says on my retirement orders: “Subject to recall’. Although if it came to that, nobody would care what we were getting paid…

The more I think about retiring early in life, the better I like the idea of “trial retirement”. I’ve never been bored during retirement, but others would quickly figure out whether they could be responsible for their own entertainment or whether they’d need to seek comfort from the workplace environment.

I definitely wouldn’t fear running out of money in early retirement, but I would definitely fear not finding enough to keep me productive and sharp. I like to think I’ll be able to keep my routine mostly intact, but my guess is that by taking away the pressure of spending 11 hours a day away from home working, I would end up wasting a lot of productive time. Has that been your experience at all?

It’s hard to say how “productive” I am since I left the working world and have taken over full time child care duties for 3 kids, one of which is 1.5 years old. So to summarize, I don’t feel very productive at the end of the day, but diapers get changed, kids are fed, delivered to school on time, picked up on time, generally properly clothed, etc.

I have plenty of things to keep me “productive and sharp” and in fact have too many things to do and I never seem to accomplish them all. I actually have to intentionally focus on slowing down, sitting back, and propping my feet up. Otherwise the relaxation time seems to be hard to find if you don’t focus on relaxing.

Justin, one year into retirement I’ve also found myself having to do too many things, not too few. So much so, that I’ve instituted a daily “time budget.” What I call have-to-do’s get 4 hours of my time in the morning and 2 more in the late afternoon/early evening (paperwork time). But the rest of each day’s time (in a nice, big block) is reserved for my want-to-do’s — like hiking, doing my blog, reading, playing strategy pc games, and taking extension/video courses. Oh, and at a minimum one day a week is designated as “Free Day” — no have-to-do’s at all, if you don’t count cleaning the kitty litter box!

That sounds like a good strategy to make sure you are focusing on the right things every day. I don’t have a formalized routine like that, but I’ll set small goals like “finish X by lunch” or “read for 2 hours”. I’m usually decent at accomplishing mini goals like this, and with a toddler running around the house, it’s about the most structure I can afford. He likes to tell me what my schedule is.

What Justin said. My spouse and I retired with a tween in the house, and now that we’re empty nesters it feels like a honeymoon all over again.

The cliche is that “But… what will I DO all day?!?” is one of the top three worries of every early retiree. (The top two are inflation & healthcare.) Six months after retirement, everyone wonders what the heck they were worrying about.

Running out of retirement is one of the single biggest concerns I have about one day entering into early retirement. I don’t sweat the small stuff. What if there’s a major medical problem, a lawsuit, a disaster and insurance decides to jerk us around? You obviously can’t prepare for everything from every angle, and the possibility of all of those things is pretty small. But take this weekend for example: Within two days we had to take our car to the garage to get fixed for an emergency repair (+$400). Then we had a huge snow storm that wiped out power to every house in the area, and we had to rush out to buy a generator (+$800). There’s $1200 I wasn’t planning on spending, and those weren’t even very big ticket items!

However I do take a lot of comfort in having options similar to what you’ve laid out. I too also plan to spend on a small fraction of my fortune, count on dividends/interest that are semi-guaranteed, and leave myself the option to continue earning money through my own ambitions.

I’ll have a HUGE post on this out-lining my entire plan next Monday. I think you’ll enjoy it!

Awesome, send me the link or tweeter it to me on Monday. I’ll give you my professional review for free (ha ha)!

I know what you mean about the “emergencies” that come up. A lot of those smallish emergencies are cooked into our $32k budget since it is based on 3 years of historical spending (that I tracked to the dollar). Appliance replacement and repairs, home repairs or major maintenance, major car repairs, childbirth, insurance rates went up, etc. Those are all expected “emergencies” so I would hesitate to even call them emergencies, and just plan on spending something on those types of things each year. I added in $1500 extra to cover house related repairs/replacements that will be necessary occasionally.

I put something like an extra $1000 to cover the “unknown unknowns” that might arise. That obviously won’t cover much of a major medical problem or a lawsuit, but how do you really plan for those anyway? If it was an extremely expensive catastrophe that imperiled our long term early retirement plans, and I needed hundreds of thousands of $$ to get back on track, I’d just hang up my ER spurs for a few years and head back to work.

Better to enjoy life now while you’re young and healthy (with an adequately sized portfolio to handle almost any likely contingency).

Great post! Thanks! 🙂

I really enjoyed this article, Justin. It addresses a lot of the common fears we face en route to FI.

Awesome post/blog. And by the way, that nightmare is not limited to those already retired… early or not.

I too am a North Carolinian… be a bit more quiet about that so we can keep the secret please???? Laugh…

I always suggest to people that owning their residence when entering retirement is a beautiful way to dramatically reduce and control spending since its the biggest monthly outlay for most folks.

Keep the great content coming..

A new fan.

North Carolina sucks and it’s really backwards. Don’t ever move here. It’s hot and muggy in the summer and in the winter everything shuts down for a few days if we see snowflakes. How’s that for an anti-Chamber of Commerce message? 😉

Owning your own residence in a place like NC where it’s cheaper to own than rent is a great way to “fix” most of your housing costs and ignore inflation on at least part of your budget.

Laugh… don’t forget it’s not very family oriented and strangers you see on the street NEVER say hi…

How could I neglect to mention those negative points about NC?

It’s funny how when you, “retire” all of a sudden your find all of these income streams that weren’t at your disposal before 🙂 I think that happens naturally as the person shifts away from the “career” they once had and instead naturally engages in work that is fun and exciting!!!!

Who cares if that also happens to make money (it often does)?!?

Long live North Carolina (I love it here as well)!!!! 🙂

I feel a summit forming…

Where are all you guys located? Near Raleigh?

I live near Davidson, North Carolina. You know… 20 minutes – 2 hours north of Charlotte (depending on traffic)!! 😉

Sounds like you’re good friends with I-77? 😉

Pardon me while I date myself, but I remember the Cornelius exit off I77 when there were really only Ham & Eggs and McDonald’s as fine dining options…

@Nate

I’m in for a meetup.

I live in South Charlotte (plus I just moved back to NC from Florida a couple of years ago), so I’m not the best authority on Clt generally or uptown/north clt specifically. I have a couple of friends who live north of uptown. I can dig around and see what they like.

S. Clt is great… and there are tons of neighborhoods. If you want to split the difference between Uptown and suburbia, Dilworth is good. Nice mix of neighborhoods and you would LOVE the commute.

Charlotte for me… but I used to live in Raleigh and I left on good terms… I think…

Haha!! Justin, I77 is my best friend unfortunately… Do you live in Raleigh? Thankfully I discovered an express bus that shuttles back and forth from Huntersville and Uptown Charlotte. It costs about $100 a month, keeps miles off the Lexus and gives me the opportunity to meet new people everyday. I love it!!

@TAOST – do you live directly in Uptown? Any standout recommendations for neighborhoods/areas to live? I have several clients in the city and we have been considering a short-term (12 month?) move in order to eliminate my 2.5 hour roundtrip commute when I am not working remote. Maybe Justin can host a meet-up, I’ll by lunch and pick your brain 😉

You got it! Why not make some money doing something you like anyway? Or at least keep your mind open to that option in the event you might need some money during early retirement. Who knows, you might find a new calling that’s completely enjoyable and rewarding.

I had the inflation and losses questions but I see that you answered them already. The biggest take away here is that you can work hard for a few years and sock away enough cash that you don’t need to work until the end of your life to enjoy it. Have fun with the kiddies.

Running out of money is a great fear for all retirees early or not! I think if you’re good enough with your money that you’re able to retire early, those skills should keep you in pretty good shape when you do retire.

I’m afraid of running out of money. That’s why we don’t plan to dip into the principle until we are well into retirement. I’d rather work part time than withdrawing now.

If you’re comfortable working part time, that’s a great strategy to keep your skills sharp and keep the cash flowing into your accounts!

Once my kids are on auto-pilot a bit more (like when the almost 2 year old is potty trained and in K or 1st grade), I might pick up something very part time. Or focus more on the blog or do some freelance writing. Right now, time is still at a premium for me!

One thing that this article did not discuss that I would worry about would be health care expenses. As we age these costs go up dramatically. How do you plan on dealing with these situations?

In short, Obamacare. At our income levels, we’ll qualify for a fairly large subsidy. Here’s a quick look at the subsidies and what we might pay: https://rootofgood.com/obamacare_makes_early_retirement_easier_and_more_secure/

At the lower income levels, they also offer low out of pocket maximums to keep the costs limited (the “Affordable” part of the Affordable Care Act).

Before Obamacare, healthcare was the huge unknown for early retirees. Now there is so much less uncertainty. Costs might rise over time, but at least we can have some level of certainty.

And I don’t really know if working provides much more of a solution, since I’ve seen plenty of employers stick their employees with a large share of the insurance premiums. My last employer charges $8000 per year for basic family coverage (you pay 20% after a sizable deductible). If you work, you continue to earn enough to cover the premium and any increases, but it can eat away a big chunk of your paycheck.

I guess if you retired early and ran out of money and were able bodied you would be able to go back to work and work for longer. The only thing is you’d have less time to invest more retirement savings.

That’s the way I look at it. I can always return to full time work if the portfolio goes crazy and more than half my portfolio is gone. Less time to save for retirement, but less years of retirement to fund as well.

I find your level of confidence about being able to just jump right back into employment both admirable and scary. If you’re out of the work force for too long you lose your competitive edge and will probably have to take a rather low paying job with few, if any, benefits. I’m new to your site so maybe I’m missing some critical information. Running out of money is my biggest concern about retirement – early or otherwise. And I don’t share your confidence in Obama care. Health care costs are unbelievably expensive – both my in-laws lived in nursing homes for years and needed extensive medical care. Yikes – that’s scary. Having raised a couple of kids, I’m curious what your game plan is should any of your children get ill or have a horrible accident – what about putting them thru college or even high school sports, etc? That stuff isn’t cheap.

Jim, Thanks for stopping by and digging in with some good questions. I’ll try my best to answer them fully!

Here’s an article I wrote about taking a long mid career break or sabbatical. To summarize, getting back into the workforce isn’t impossible. For me and my wife, we aren’t leaving extremely high paying jobs. The job I left only paid 16% higher (after inflation) than my first professional job post-college. In other words, replacing my income with an entry level position in my field won’t be that difficult. We only spend $32,000 per year, and starting salaries in engineering are higher than that. Even an engineering technician’s salary is usually that high.

Healthcare: We have $48,000 set aside in a Health Savings Account. We spend very little right now on healthcare (recently $1,400 per year average on med/dental). For the retirement budget, I included an extra $2,000 to allow for $3,400/yr med/dental expenses (check out the retirement budget here). Our HSA can also be tapped if we hit unexpected medical expenses. The HSA also earns a decent amount of money on its own (it just paid $800 in dividends on December 2013, for example). Nursing home expenses? We don’t have anything specifically set aside for those. We are still in our 30’s and have (hopefully) many decades before that is a concern. We spend so little from our portfolio that the odds are the portfolio will grow over time. What will non-millionaires do for nursing homes in their old age? Something’s got to give.

As for Obamacare, we’ll see how it plays out. Amazingly, every other industrialized nation has some form of broadly available health care, so whether we continue having Obamacare or some other program, I think our household will continue to enjoy access to healthcare. And if healthcare isn’t available through the exchanges (ie Obamacare goes away), we can always get jobs just for the health insurance. Or enjoy the private health care that is much more affordable overseas (Thailand or Mexico, for example).

My quick and dirty analysis says it doesn’t make sense to continue working an extra decade or two to cover the “what if” of lack of access to healthcare. We are vastly more wealthy than the large majority of people in America, so I don’t think we’ll face the struggles alone. We’ll shake and hustle when the need arises. In the meantime, I expect we’ll enjoy the next couple decades without worrying too much.

Kids’ college: We have dedicated 529’s that are funded with about 2 years worth of in state tuition for each kid. We can pay the rest out of our other investments. They might get scholarships, grants, loans, or have money from work-study or summer jobs during high school and college.

You’re correct that there are risks to retiring early. Running out of money is one of them. But as I explained in this article, there are plenty of ways to mitigate those risks.

Great post. This was very well written, and kudos to you for being able to keep your expenses in check. The 3-4% rule for retirement is just a guideline, and for you to be even lower than that bodes well for your retirement success. Plus, as you pointed out, it’s so important to do a gut-check if the markets pull back and changes need to be made (short-term or not). Who knows, maybe there could even be some short-term income solutions too that you could pursue to help subsidize your expenses if markets don’t perform well.

I’m feeling pretty good about our prospects. Having multiple lines of defense and remaining flexible will get you a long way.

This article is really motivating. I have interests of trying to retire by age 40 (currently 32 now) and so many people ask the two questions: what will you do all day and what if you run out of money? I think you’ve answered both of these questions expertly! I’m one of those folks that has a very hard time sitting in the office all day and would really enjoy additional freedom. Also, so many people are brainwashed into taking almost zero risk that they waste most of the best years of their life away in the office vs living them to their fullest 🙂 Again, very inspiring article, thanks!

Thanks for visiting, MoneyAhoy! I wish you luck in your goal to retire by age 40. Luckily you have 8 years till you hit that goal.

What will you do all day and what if you run out of money? How about competing risks to put it in perspective? What if you keel over your desk from a massive coronary and never get to live the life you wanted? What if you spend your entire kids’ childhood working all the time and never have much time or energy to devote to them?

Whatever bad things end up happening to you, there’s always risk. But the possibility of something negative occurring (running out of money or getting bored) doesn’t mean you shouldn’t put efforts in place to grow wealthier over time. After all, wasting all your money on crap today doesn’t lead to risk. It leads to 100% certainty that you’ll never be wealthy enough to retire ever! 🙂

Great article. I am a little late finding it but just wanted to comment that it is nice to find another early retiree that doesn’t consider it a retirement failure playing by our own rules and staying open to pursuing employment or as I call it, pursuing opportunities. The mindset of being able to call your own shots and do whatever you want to do is my idea of retirement. After all the years of planning, saving, and living below our means, we know our chances of a fulfilling and deserved early retirement and we shouldn’t allow fear of running out of money hinder us from living the best life we can on our own terms. Thanks again for a great article.

Hey Tommy! Thanks for stopping by Root of Good.

From looking at your site, I can tell you “get it”. It’s relatively easy to make money and fund a life of leisure. Sure, there might be risks along the way, but you get to set your own rules in early retirement.

I’m at that point financially where I can actually stand to take a little MORE risk with some of my portfolio since I can afford a little failure. And I can take on any type of work (or none at all). It’s a nice spot to be in!

Great article. There are always a ton of possible safety measures to insure you’ll never run out of money. If history serves us well, you’ll be fine 🙂

I think so, too. But there’s always that worry that we’ll be in the 3-5% of “failure” scenarios. That’s why flexibility is important for the 30-something early retiree.

(sorry it took a few days to approve your comment – it got caught in the spam folder with 898 other spam messages. Your comment and Jeremy’s comment from Go Curry Cracker got eaten for some reason.)

My take on the future costs of healthcare: Medical arbitrage = having your medical procedure done in a much cheaper destination like Mexico, Peru, or Thailand. Doctors and dentists have to maintain high levels of malpractice insurance and association fees which drives up the cost. I just read in a Marketwatch article that medical tourism has been gaining popularity and many US trained Doctors are moving abroad to avoid all the mandatory cost of maintain a practice in the US. In the same article it listed the price of a knee replacement in the US was $25k whereas Mexico was roughly 12k.

Here’s how I would do it:

1. Save a much as possible in your HSA

2. Build up some miles on your travel card

3. Rent an apartment for a few months in your chosen medical destination (for your research/recovery)

4. Do your research to find the right Doctor

5. See if you can bundle your services to reduce your cost of traveling twice.

6. Look for additional tax deductions if your medical costs exceed the 10% cap (if this still exists)

I plan to do this for my dental care as dental costs are outrageous in the US. An implant is $3500 for one tooth. Why pay for a crown ($2500) that is only good 10-15 years when you can get an implant that lasts a lifetime? I also plan on checking into orthodontics which is likely to be cheaper overseas.

You’re right on with this comment! We haven’t done any medical tourism so far, but I wouldn’t rule it out. I have heard about costs that are 25-50% of what you would pay in the US with US-trained doctors and dentists providing the services. I certainly don’t think there is anything magical about US soil that grants medical providers special powers that aren’t available outside of our borders, and while it pays to check out providers wherever you are, there’s no reason to fear medical/dental care overseas.

Just want to let you know that the town of Algodones Mexico across the border from Yuma, AZ offers cheap high quality dental care. Think $130 for a crown. It is safe and you can even stay in Yuma and cross the border as needed.

Good to know, thanks. It’s 5-8 times that expensive in the US I believe.

That’s not possible. The gold alone in a crown would cost more than that. Is this magical thinking?

I retired at 39. Failed one year later. I invested $250,000 in a scam.

The full story is here:

http://www.awolgeordie.com/2014/10/how-i-lost-250000-with-centaur.html

I did all the minimalist stuff. High savings rate. Wrong Financial Advisor.

Be careful out there people.

Definitely the kind of thing I’d be very wary of investing in. Any time I see guaranteed returns exceeding what US Treasury bonds (or UK-govt backed bonds, in your case), it raises a red flag because there’s always risk involved. It also shows the importance of diversification. I might put 5-10% of my assets into alternative asset classes (after doing TONS of due diligence) but so far haven’t gone this route because of the risks and lack of interest in conducting the due diligence.

What are your plans now that you’ve lost essentially all of your retirement savings?

I started teaching maths again. Just turned 43 and landed a gig in China where I aim to bank $2k/month over the next few years. Aiming for retiring at 50 now. The key thing is to learn from your mistakes. One of the reasons I wrote that post was to warn others. I have since learned more about investing (eg. simple DIY ETF portfolios etc. ).

Thanks for your reply. This is a great blog. I wish I’d read it pre-2011!!!

Glad to hear you landed on your feet. Those simple low cost ETFs are amazingly easy and safe strategies to generate good long term investment growth.

I don’t fear it more than someone still working that fears they may lose their job… sh*t can happen to anyone.

And risk-wise if anyone’s retirement savings are cut in half then it’s likely due to the market tanking and surely millions of people losing their jobs… but you will still have half of your nest egg…

That’s my line of thinking. Worst case is still pretty good for the early retiree that loses half their savings. 🙂 There are worse things than having $500,000-$700,000 or so and a paid of house (in my case).