Dividends are a popular source of income in retirement. We rely on them for a part of our annual living expenses. Dividends provide a relatively steady stream of income regardless of the fluctuations in the stock market.

It’s worth stating that I’m not exclusively a dividend focused investor. Instead I focus on the total return of my portfolio. I’m an index fund investor with a fixed asset allocation that I use to periodically rebalance my portfolio. Right now I’m almost entirely invested in equities through mutual funds and ETFs. All of those investments pay dividends ranging from 1% to 4% per fund.

In 2015, we received a total of $28,527 in dividends from our portfolio. This is down slightly from the $29,437 we received in 2014. This drop was a little unexpected but owes to lower dividend payments from international investments due to the appreciation of the dollar and generally less favorable economic conditions overseas.

Our 2015 dividends were still significantly higher than the $22,000 dividend income we received in 2013. I’m going out on a limb by guessing that 2015 is a temporary lull in the long term growth of our dividend payments (assuming we don’t eat into the portfolio principal too much).

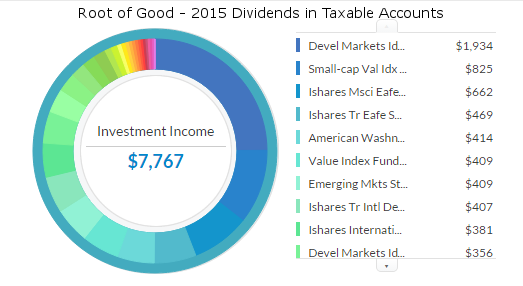

Here’s a pic from my Personal Capital account showing the total dividends for last year and how much each mutual fund paid (isn’t free automated investment tracking great?).

Around 75% of our investments are tied up in tax advantaged accounts. Accessing these funds requires some fancy financial footwork (namely, the Roth IRA Conversion Ladder), so we’re only spending the dividends in our taxable brokerage accounts for now.

This year we received $7,767 of dividends in our taxable accounts. That’s down roughly $1,300 from 2014’s $9,077 in dividends in our taxable accounts.

The $21,000 or so of dividends in the tax deferred accounts gets reinvested automatically.

The $7,767 of dividends from our taxable account covered about a third of our $23,802 living expenses in 2015, which goes to show just how important dividends can be to fund a successful early retirement. We didn’t spend our whole $32,400 early retirement budget in 2015, but our taxable dividends would have covered a quarter of our planned expenses for the year.

Here’s a summary of all our dividend paying investments:

These are the actual dividends we received for the investments in each asset class in 2015. To calculate the dividend yield, I divided the dividend payments by the value of the investment (as of January 8, 2016).

I have about $63,000 invested in proprietary index funds in my 457 account that don’t pay dividends. These funds automatically reinvest dividends internally without making a dividend distribution inside my 457 account. I took those account balances out of the denominator when calculating dividend yields.

I excluded about $40,000 in the kids’ 529 accounts because they are also proprietary funds that automatically reinvest dividends internally.

Taking a look at the chart, you can tell that the value tilted investments tend to pay a higher dividend yield. The US small cap asset class offered the lowest dividend yield at 1.51%, while the US REIT asset class yielded almost 4%. The overall portfolio yielded 2.44% in 2015.

For those wondering exactly what funds I invest in, take a peek at that “Representative Holdings” column in the chart. It’s not every single fund I own but it is a good reflection of what’s in my portfolio. Some of the funds are Ishares ETFs that trade for free in my Fidelity account, and might not necessarily be better than the Vanguard equivalent ETF’s (so do your due diligence on expense ratios, average bid/ask spread, average volume, and average variance from NAV).

The rest of this article is excerpted from my original article on dividends from January 2014 (with some updates), so for the twenty seven loyal readers that remember the original article verbatim, my apologies. For the other few thousand new readers, here’s what you missed two years ago:

Benefits of Dividends

In addition to being a good source of cash flow, dividends have a lot of other benefits, too.

Tax free income – If you are in the 15% tax bracket or lower, all of your qualified dividend income is tax free. For US funds, virtually all of your dividends will be qualified. For international funds, typically around half to two thirds of your dividends will be qualified dividends (with ordinary income tax being due on the non-qualified dividend income). Dividends can be a pretty sweet way to fund your retirement expenses since you could potentially enjoy a fairly high income yet pay zero federal income tax.

Psychology of automatically receiving dividends – In early retirement, you might worry excessively about selling in a down market and how to fund next month’s expenses. When markets are in the dumps, dividends can provide pain free cash in your pockets! They keep arriving (for the most part) in good markets and bad. Unless your portfolio’s yield is higher than your withdrawal rate, you’ll still have to sell some of your holdings to fund your monthly expenses, but having a large part of your expenses automatically funded by dividends can make it less painful.

Long term growth of dividends – The dividends paid by the stocks and funds you own will increase as the underlying companies grow their profits over time. The growth in dividends will keep inflation at bay. Dividends can grow faster than the rate of inflation, thereby providing a real increase in your standard of living.

Emergency funds – If you hit a bump in the road and need an extra source of cash before you reach financial independence, you can consider your dividends as a source of emergency funds. At a 2% yield, a “modest” portfolio of $100,000 can produce $2,000 of dividend income per year. I was lucky to never need the extra cash while working, but when my job suddenly ended and I decided to retire, it felt great to know I had an instant source of about $8,000 per year with a few clicks.

Dividend focused portfolios

If you want to become a dividend investor, you could copy my asset allocation and get a 2.44% yield without trying very hard.

Or if you want to be a hot shot investor, you can try to hand pick the “best” dividend stocks out there and craft a portfolio that pays 3-4% or more. I’m not particularly good at picking stocks so I wouldn’t personally choose this route.

I like easy solutions that don’t take a lot of work. Vanguard has a few excellent offerings that are dirt cheap (which is a good thing when you are shopping for an investment).

The Vanguard High Dividend Yield Fund is available in mutual fund or ETF format (ticker: VHDYX or VYM respectively). The ETF version (VYM) has a nice low expense ratio of 0.10% (which is great!). This fund invests in stocks that consistently pay higher than average yields today. The fund yields about 3.4% currently.

You can sacrifice a bit of yield today in exchange for higher dividend growth in the future with two different Vanguard funds. The Vanguard Dividend Appreciation Index Fund (ticker: VDADX for mutual fund or VIG for ETF) is the better choice since it has a low 0.10% expense ratio and a current yield around 2.3%. The other option, the Vanguard Dividend Growth Fund (ticker: VDIGX) comes with a higher expense ratio (0.29%) and a 2% yield.

Another great way to put together a dividend focused portfolio is by purchasing a basket of solid dividend paying stocks through Motif Infesting (full review here). For $9.95, you can buy a slate of up to 30 stocks. You can choose your own 30 stocks based on your own dividend screens. For example, you can set a filter that shows only those stocks with yield over 4% with a history of stable and growing dividends. Or you can pick from one of Motif Investing’s many pre-selected “motifs” (basket of stocks) centered around high dividend yield or dividend growth. Buying motifs is slightly more complicated than buying a dividend mutual fund, however you can skip the 0.10% to 0.29% expense ratios by owning the stocks directly. That means a 3% yield after expenses would become 3.1% to 3.29% without the expenses. Definitely worth checking out Motif Investing if you want to maximize your yield.

Parting Thoughts

Dividend yields can be a great way to generate cash to fund an early retirement. I personally don’t put too much emphasis on dividends in my own portfolio, since I’m expecting long term appreciation of my investments to keep me flush with cash as I continue to enjoy my early retirement. But a 2-3% dividend yield can fund the majority of your budgeted retirement expenses if you don’t exceed a 4% annual withdrawal rate from your portfolio.

I came of age and started buying my first investments during the roaring 1990’s tech bubble when everyone was making easy double digit returns and no one cared about a few percent yield. The focus was all growth growth growth, and sometimes profit profit profit was ignored. After the tech bubble burst and double digit losses replaced double digit gains, the dividend investors sat back and smiled since their dividend focused portfolios sailed through the crash relatively unscathed.

A decade later, the old high growth tech bellwethers like Apple, Microsoft, and Intel have become somewhat boring dividend payers (yes, Apple is boring).

Some companies are good at consistently earning money but still don’t pay any dividends at all. Warren Buffett’s Berkshire Hathaway is one of those companies. Mr. Buffett thinks it more efficient to reinvest all the corporate earnings from Berkshire’s holdings instead of giving part of the earnings to shareholders in the form of dividends. Berkshire Hathaway’s impressive track record of outperforming the S&P 500 by 4-5% annually for a few decades means Mr. Buffett knows what he’s doing.

I mention Berkshire Hathaway’s solid investment performance to highlight a company you would completely miss if you were strictly a dividend investor.

Dividend focused strategies can pay off, but so can investment strategies that are spread across many asset classes.

What is your take on the dividend investment strategy? Do you manage your portfolio with a focus on generating current dividends growing your dividend stream in the future? Or do you rely on the overall growth of your investment portfolio?

Root of Good Recommends:

- Personal Capital* - It's the best FREE way to track your spending, income, and entire investment portfolio all in one place. Did I mention it's FREE?

- Interactive Brokers $1,000 bonus* - Get a $1,000 bonus when you transfer $100,000 to Interactive Brokers zero fee brokerage account. For transfers under $100,000 get 1% bonus on whatever you transfer

- $750+ bonus with a new business credit card from Chase* - We score $10,000 worth of free travel every year from credit card sign up bonuses. Get your free travel, too.

- Use a shopping portal like Ebates* and save more on everything you buy online. Get a $10 bonus* when you sign up now.

- Google Fi* - Use the link and save $20 on unlimited calls and texts for US cell service plus 200+ countries of free international coverage. Only $20 per month plus $10 per GB data.

I like your approach. In the modern era I don’t like dividend investing. Companies are now choosing to do stock buy back programs to boost stock prices and return capital to investors that way. As such, I don’t think anyone should be strictly a dividend investor in the modern era as it will become more and more rare for companies to pay dividends.

I’m mainly afraid of missing out on the good companies that don’t pay dividends or pay a very average dividend and therefore wouldn’t be included in a dividend investing strategy. Instead, I like owning the whole market.

Is this dividend portfolio still your entire holdings today in 2021?

Yes, equities portfolio remains unchanged but now it is only 90% of overall portfolio. I also have a 10% bond slice.

“Psychology of automatically receiving dividend” – for me, that’s huge. Our portfolios have fallen across the board the last month, like everyone else invested in equities, but I give myself a little bit of a psychological boost when I remember two things – timeline and purpose.

My timeline on my index funds is to not touch them for many many years, certain longer than the trough to peak return of the equities after the SUP500.

The purpose, which means dividend income from the dividend stocks and funds, will still continue to produce. With the exception of energy (i.e. oil companies), the other dividend stocks are still doing well despite their stock price. They’re unlikely to waver in paying out the dividend, so unless I sell my stock and lock in the losses, I haven’t “lost” anything.

These two ideas kept me invested (and continuing to invest) during the downturn and now through this “hiccup.”

FWIW, the third thing that keeps my head in the right place is knowing I’m just giving back some of the massive gains of the last few years. 🙂

I totally agree with Jim.

Any time a dividend payment is paid to me, it also serves as a kind of positive reinforcement that helps me reiterate to myself that I am a partial business owner of tens of companies in a variety of industries that have global operations and employ millions of workers. Those companies earn profits, and share a portion of those profits in the form of a cash dividend. The stock market can value those businesses any way it wants, resulting in fluctuating share prices. But the cash dividend provides investors like me with a positive reinforcement to hold on to their investments during market declines, and ignore those stock prices.

And when you ignore those prices, and focus on the stability of cash dividends, you can afford to stick to your long-term investing plan through thick and thin.

And when stocks go down, it truly does represent a sale as long as the prospects of the company remain strong (and the dividend isn’t at risk). You get the same dividend, a higher yield, and the payments reinforce the good behavior.

Definitely a great point. The consistency of the dividends helps us remember that what those shares represent is a tiny fractional ownership in a company. And those companies often still generate profits even in a bad economy when the stock price is way down.

“the third thing that keeps my head in the right place is knowing I’m just giving back some of the massive gains of the last few years.” I console myself with this same knowledge. 🙂 The market goes up, it goes down. Right now it’s gone down, but not nearly as far as it went up.

Hi,

I am curious how you get Dividends as a separate dashboard (root of good – 2015 dividends in taxable accounts) in Empower.

In my Empower dashboard I see “Dividend:Stock ABC” in the Description and the Category is OTHER INCOME.

Do I check all my Dividends and the change the Category to “Dividends Received” ? or is there another way?

I’m not sure. I think you can drill down to a specific category of income. I do review my transactions monthly and make sure all the income is properly categorized.

Love the dividend growth investing strategy and it’s our primary plan for reaching financial independence. Most of our dividend focused holdings are in taxable accounts and then we have another good chunk invested in mutual funds in a 401k/Roth IRA/Rollover IRA. Dividends do provide a nice fall back whenever the markets are pulling back like they’ve been to start off 2016. The good thing though is that reinvested dividends are buying more shares now.

Yes! If you’re still working and accumulating assets, then those dividends are buying even cheaper shares now.

Great article. I would be concerned about focusing solely on dividends, but your approach seems very reasonable and part of a larger strategy. Only having to withdraw $14/year in principal from your taxable account seems very sustainable, especially using index funds with low expense ratios. Certainly good enough to tide you over until the taxable accounts become available more easily.

It’s certainly nice to get these dividends right now, given how the market is in a slump.

Like you I focus on total return. The dividend yield from my mutual funds in my brokerage account will be a nice asset in FIRE if I decide to find part-time work or projects that pay, as it will eliminate the need to worry about selling mutual funds. But at the end of the day if you’re living off a 4% portfolio dividend yield, you’re still essentially doing the same thing as someone with a 2% yield and selling 2% each year. It’s basically the same thing.

That’s right – the bottom line is that a 4% dividend yield is the same as a 2% yield from less dividend-focused stocks plus selling 2% of the principal. Some companies simply reinvest more of their earnings while others pay out a significant part of their earnings.

Tax-wise, a 2% yield and selling 2% of principal is better than a 4% dividend yield. Quote from paper published by Vanguard:

This reduction (in tax rate on qualified dividends) led many investors to believe that there was no difference between the taxation of cash flows on qualified dividends and the taxation of capital gains. Not so: While it is true that the 15% tax rates are identical, the amounts that the tax is applied to are not. That is because a qualified dividend is taxed at 15% in its entirety; whereas if the equivalent sum is realized from a stock sale, the 15% capital gains tax will apply only to whatever portion of the sum represents a gain. As a result, both pre- and post-JGTRRA, dividends should be avoided from a tax perspective.

That’s a great point, and one I haven’t overlooked when it comes to raising cash for the year’s living expenses and also keeping an eye on ACA subsidies and your AGI and setting up the Roth IRA conversion ladder. The sale of appreciated shares equates to less AGI than if that income came in the form of dividends, since part of the sale is your basis or return of capital.

Thanks for this article – I haven’t concentrated much on dividend income as part of my portfolio until this past year. Unfortunately, I had the mindset of picking stocks that I thought would increase in value (that’s a gambling man’s method!). I now look more at the passive income (dividends). I think Dividend Mantra was my big wake up call on this.

I’ll definitely check out the Vanguard funds you suggested.

— Jim

Those Vanguard funds are great places to start, particularly the ones with 0.10% expense ratios. I don’t follow a strict dividend focused investment strategy, but if I did, one of the VG div funds would be the core of my portfolio, with some nicely paying blue chips for a shot at some extra yield.

Very timely article and just shows that investing in index funds can still bring in good amount of dividend. I’ve been focused mostly in individual dividend paying stocks but lately have been purchasing some index funds to diversify our exposure. When it comes to dividend and index fund, you aren’t sure exactly how much yield it’ll produce, so it becomes slightly harder to estimate your income level. I’m like you though, heavily invested in tax-sheltered accounts. The plan is to maximize tax-sheltered accounts first before investing in regular accounts.

I like the idea of diversifying with index funds. It scares me to see some dividend investors who are concentrated in 15-20 issues, with half of those representing the large majority of the portfolio (and often in the same sector!). Scary stuff if a sector gets smashed (a la banking 2008 or oil today).

Wow, for a “non-dividend” investor, you sure make good dividend income (it even easily covers your cost of living!). A 2.4% yield on index funds is actually remarkably good. As you noted, it makes you sleep even better at night 😉

It’s the value tilt and the international investments. Those tend to pay higher than average dividend yields. But I have to admit, pure accident.

Thanks for sharing. We have about $300,000 in our exclusive dividend portfolio. The rest are in index funds. The dividend portfolio pays off more dividend because that’s the focus of that account. The dividend portfolio will help fund our early retirement when Mrs. RB40 retires. The index fund in the retirement accounts won’t be touched until our late 50s or early 60s.

2.4% is very good for index fund. I suspect 2016 will be a tough year for dividend. Energy companies will probably have to cut dividend and some other sectors might follow suit.

I’m curious to see how dividend will turn out in 2016. I’m assuming flat or lower….

Wow, you have 50% in international. That’s a lot. 2015 was a rough year for emerging markets. Hopefully, the international markets will come back in a few years.

Let’s brace our self for 2016. 🙁

I’m guessing flat to down for dividends, especially in my 50% international portfolio. And yes, it was a rough year for international, especially emerging markets. The good news is I rebalanced into more emerging markets at a relatively low point.

I have a mixed bag of investments. Some individual stocks, some mutual funds, and some ETFs spread across my accounts. I have been moving to more ETFs as I don’t have time to research stocks right now. I hold a couple of companies I think are really great, but they are also top holdings in most funds, so it is a bit redundant.

I have tried to balance overall and not in each account based on where I can get the lowest fees. For example, the international fund in my 403b/457b has a very high expense of something like .60%. I think people sometimes try to balance in each account and don’t get the best overall rates they could when having taxable, roth, ira, and 401k accounts to manage.

I do the same thing with finding the best (lowest cost) investments in a particular account and just buy those. My 457 is a good example – limited low expense options leaves me investing in only Total US index and Total International Index at 0.10% and 0.20% fees respectively. That’s almost double what I would pay for a similar Vanguard Admiral fund or ETF, but it’s better than the 0.6-0.7% actively managed funds that consistently underperform the index funds by 0.5% or so (just about the exact difference in fees 🙂 ).

VDADX/VIG is a great one click way to get dividend growth exposure, glad you noted that.

I rely almost entirely on passive income in FIRE and that includes a healthy allocation to debt and debt like instruments. The low volatility helps me sleep during periods like the last couple weeks.

I don’t have much of an allocation to fixed income investments but still sleep at night. Check back if the market drops another 20% and see if I’m still sleeping. 🙂

Nice post on dividends RoG. Very timely with the markets in decline. As I see it, dividends are ‘business returns’ and stock prices are ‘market returns’: http://www.mrtakoescapes.com/2016/01/16/mr-markets-hangover/

We choose to live off our dividends instead of stock sales – We don’t want to sell when the markets are down. We want to buy when markets are down!

As it is, dividends may be the only kind of return we see for a year or two.

That’s certainly possible that we won’t see much in the way of market returns over the next couple of years. Which is okay given the growth since 2009. Slow and steady suits me just fine.

The last few weeks, I have been thinking on dividend investing, but without having the need to do all the research and follow up myself. The article you have here is – at first sight – the way 2 go for me.

Living in Belgium means I have to take into account some double taxation.

It is worth while to look further in this.

AT

Lots of European companies pay out very nice dividends, though I believe they fluctuate more year to year compared to their US counterparts that want to pay a steady, consistent dividend year to year.

Thanks for posting this — a lot to digest.

I have an initial (and probably dumb) question re: tax implications of dividend income. Does the dividend income itself count towards what tax bracket you are in the same as how earned income does? Or is it a totally separate category?

I guess what I’m asking is could I theoretically keep my earned income low enough to stay in the 15% tax bracket and get $500,000 that year in qualified dividends paying 0% on it. (Numbers ridiculous for illustrative purposes.)

Your qualified dividend income adds to your regular income for tax bracket purposes. In the $500k of div income example, you would be in the top tax bracket paying 15% on most of the dividends and the max rate on your ordinary income.

Thanks — I actually did some research on this today while killing time on boring conference calls. It did seem too good to be true the way I initially envisioned it.

But, you could still get a very high income on qualified dividends with a pretty low marginal tax rate. Which, I suppose is what Buffett was describing when he said his tax rate was lower than his secretary’s. I’m not sure what I think the tax system should ideally be — but it certainly makes sense to optimize my own situation to take advantage of the system as it stands.

Right on – Warren Buffett could get billions in qualified dividend income and pay 18.8% while regular middle class people can pay a 25% marginal rate (on the last dollar).

The really sweet spot is a single person being able to receive almost $50k in qualified dividends at a 0% federal tax rate.

I like what you were able to do with Personal Capital’s tables and charts. Unfortunately, I’m having a lot of trouble with Personal Capital mis-classifying dividends as securities trades instead of as investment income. Even after I correct the classification, the program will not reclassify for purposes of totaling investment income.

I can’t trust or rely on Personal Capital’s accuracy which undermines the utility. Have you had problems with that and if so, how have you dealt with them? Since you are segregating dividend income, how do you classify capital gains in funds?

Hmmm, I haven’t had a problem. I have accounts at Fidelity and Vanguard and haven’t seen any issues with those. Maybe it’s account specific? I’ll keep a look out though because sometimes transactions get a weird label if I’ve previously classified something differently.

I have Fidelity, Vanguard and T Rowe Price among others. All have been mis-classified at times. Fido and Vanguard are inconsistent and not predictable. T Rowe Price is always wrong. The dividends and capital gains do not show up at all in Investment Income. Something I will have to take up with the PC folks, I guess.

I guess I might recall a very rare occurrence of a mis-classification for dividends. I’ll go through all the transactions and double check them, and sometimes have to make a correction. Certainly not a routine thing though. And once I catch it, I have no problem reclassifying the transaction to be a dividend or sale or whatever.

We moved half into index intermediate bond funds. Stock index went down 7’percent. Bonds were up 1.25.

This could be a dumb question, but should I be counting the capital gains distributed from my mutual funds as dividend income? Most of my funds pay short-term, long-term, and income. Which of these should we be counting towards investment income received?

I would count only the dividends as true income if you’re trying to figure out what a mutual fund’s dividend yield is. The cap gains will vary a lot year to year and are really just an artifact of our US tax code that requires the funds to pay out any gains realized within the fund.

But in terms of looking at cash flow each year, those cap gains distributions spend just the same as a dividend payment. So from that point of view cap gains distributions are still income.

ah ok thanks. one more question – so when you are quoting your dividend figures, do those include cap gains distributions (long/short) paid on your funds? (i understand your yield calculations are only on income)

No, only dividends. Not that we get many cap gains distributions with index funds anyway! 🙂

One of the benefits of dividend income is the simplicity of it. Especially for newer investors, it’s easy to wrap your head around dividends as an income stream because it more closely mirrors that of a typical salaried job. By not having to sell off shares, not only do you not to risk selling in a low market or dipping into principal, but you have a more passive cash flow that is closer to what you’re used to from your working years.

All that said, I don’t think focus solely on dividends is the best strategy. For now, I’ll continue betting on total stock market growth and consider any dividend yield in addition to it a nice bonus.

“For now, I’ll continue betting on total stock market growth and consider any dividend yield in addition to it a nice bonus.”

That’s been my strategy all along. Corporate profits are either paid to investors by dividends or share buy backs or are reinvested into the company. It’s all the same to me (assuming reinvestment actually produces some real gains in corporate earnings!).

I remember reading about Berkshire’s choice not to pay out dividends as on relating to reducing taxable income for shareholders.

I’ve read that, too. His basic philosophy is to let individual investors decide when to experience a taxable event with BRK shares instead of pushing income onto the shareholders. Makes sense if you’re managing tax liabilities very closely and don’t need the income.

Impressive that you have a good tilt towards international funds. You mentioned that it wasn’t exactly by intention, but I guess you just had your tax advantaged accounts directed towards international?

The 50% international allocation was intentional, but where I hold international isn’t always by choice due to different availability of fund options in the various accounts we own.

Thank you for sharing your portfolio with us. I like to compare what others do with my own portfolio to see how it stacks up. It usually reveals specifics I sometimes miss.

Right now I focus on overall growth as I am about 3-5 years to semi-retirement. 8 years to total retirement…if I want.

My ideal basket looks very similar to the ROG portfolio. Right now I am deferring everything into 401K, some into Roth, and HSA accounts because my tax bill would be INSANE if I did not. I also like the thought of slow flipping houses every couple of years to unlock more capital to fund the stocks. PHYSICAL Gold and silver, in small amounts is also on my radar. I plan to hold for 30+ years…very long term, but I am convinced this the only way to play the precious metals game.

I am self employed so I like the idea of funding the stock portfolio while I’m young. When everything is well funded I can move toward business ventures and rental buildings.

I know everyone here is a reader so I thought I would share a few books that have helped me develop my investment approach:

Richest Man in Babylon

The Gone Fishin’ Portfolio: Get Wise, Get Wealthy…and Get on With Your Life, Alex Green

Unconventional Success: A Fundamental Approach to Personal Investment, David Swenson

The 7Twelve® Portfolio, Craig L. Israelsen, Ph.D

Intelligent Investor

Great book recommendations. Some I’m familiar with, some not. It’s good to see you’re taking a long term approach to investing – it will serve you well over the course of your investing career and give you a shot at good long term gains.

I’m really more focused on growth stocks to gain more principal appreciation hopefully as I’m still under 40. But as I get older, I’ll allocate more towards stable value assets, and large cap stocks with dividends.

I’ve got about $25,000 out of my $175,000 passive income portfolio consisting of dividends. The rest is rental income, CD interest income, and alternative income.

In a rising interest rate environment, dividend income stocks tend to get hit more so I’m going to wait for a year or two.

Sam

S

That’s a smart approach – let those growth stocks do their magic to generate wealth and then convert to more income producing assets later on. I may end up doing something like that if the traditional dividend payers ever go on fire sale.

I have to tell you – your recommendation of Vanguard funds is truly valuable. All of these articles talk about the kinds of things to invest in at a vague, macro level. Naming the fund is extremely helpful to those of us looking to better understand the best ways to invest. Always an enjoyable read – I find your perspective refreshing and of high value.

Thanks! I like to throw out what I actually own because it’s a very concrete example of how anyone can get a decent, diversified portfolio for relatively cheap.

Great insight. I never thought about using dividend income as an emergency fund vechicle. Many people believe stocks to be risky investments, which is true, but what most don’t understand is that dividends are generally still paid whether or not the market is down or up.

Justin,

Etfs like Vti hold a strong amount of mid cap stocks in the portfolio, you use the S & P 500…Why no allocation to the mid cap category (even a 5% allocation), just wanted your thoughts. I see lots of portfolio examples excluding mid caps.

Thanks man!

I have a tilt toward small cap stocks (more volatile, higher expected return). Return of small cap stocks are less correlated with the return of large cap stocks (SP500) so there’s some benefit to staying on the extremes of the capitalization scale.

I’m not a strict purist, and actually use VTI/Total Market and SP500 interchangeably (to tax loss harvest and switch between 2 positions that are similar but not “substantially similar” per IRS rules).

I also hold the Extended Market index fund instead of a straight small cap fund in one IRA because of the fund options available at Fidelity. Spartan Extended Market has a better permanent expense ratio than the Spartan Small Cap fund. Spartan Extended Market fund = mid and small cap, so I’m getting mid cap exposure there too.

Ok thanks man appreciate the quick response. I have a Traditional 401k in an an account at work that has high fees..so I only contibute what my employer will match. Then I fill up my Vanguard IRA that I manage. I also have a vanguard taxable account. Our belief in vanguard products as well as your allocation approach is spot on. I have a 100 k plus income and am a single 24 year old. If I am socking away 30 percent…is my next best move to throw all the excess money in the taxable account (I want to retire at 40) or am I missing something else that I could be doing?

I want to get this right sir. Your killing it thanks for any help you can give.

Yes, I’d say next best step is dumping everything in a taxable account (unless you’re planning on leaving the employer in the next few years and want to take the tax deduction today and just pay the high fees for a few years).

You’re leaving a lot of potential 401k tax deductions on the table by only doing the match. Are the options really that bad? Even with high expense ratios the tax savings probably outweighs them. You could also try to talk to your employer and see if they’ll allow you to quit/rehire occasionally so you can rollover the 401k to an IRA. Sometimes having that conversation with a valued employee can give them a hint that they need to improve their 401k options.

Justin,

I’m no hot shot investor but I do hand pick all my own stocks. Besides my Roth IRA, I buy index funds. You have an impressive portfolio. Thanks for sharing it with us. I can’t wait to be as far into the process as you are. I have just reached the $1,000 in annual dividends milestone. Very exciting to me. The road to early retirement will not be short or easy but oh so worth it. I look forward to following you.

-John

Definitely worth it in the end. 🙂

I apologize if I missed it somewhere but what company do you hold your taxable assets with and why?

Vanguard and Fidelity. Check out my recommendations page for my thoughts on the “why” for those two companies. Basically low cost and decent service.

Awesome, thanks! I’ll look into them both.

This is quite an awesome blog! We wanted to “FI/RE”. But fear of unknown(big sickness in middle age, or child’s college expenses” keep us away from that dream.

I have a few questions for you.

How do you manage to keep commissions and transaction fees low for your investments. I hate paying those. Fidelity is where we have our solo 401k, but all vanguard funds carry a 75$ transaction fee and later additions cost $5… And any ETFs other than a few fidelity cost $7.95 per trade. I feel like these eat up my returns.

Merrill Lynch has no commissions for us for individual ETFs and stocks, and probably only $20 for mutual fund. But their solo 401k is loaded with fees.

Vanguard has a good solo 401k, BUT it does not have brokerage option and I can only buy vanguard mutual funds. I prefer ETFs over MFs.

Do you have any suggestions for me? Not sure if you have discussed this elsewhere. I came across your blog from Clark Howard’s FB page yesterday and have been voraciously reading.

Thanks a lot for your time. Look forward to hearing from you!

Yoma

I have accounts with Fidelity and Vanguard. I pay $8 for most trades, though some ETFs are free at Fidelity, and all Vanguard ETFs are free at Vanguard. Mutual fund trades are free for me at Fidelity and Vanguard (only trade the Fidelity and Vanguard MFs at the respective brokerage).

Why the preference for ETFs over mutual funds? I have my solo 401k at Vanguard and it’s been great and hasn’t had any fees (though I have other assets there, so maybe that helps).

Thank you! I prefer ETFs because of paperwork involved with 1099B in taxable accounts when it comes to MFs. ETFs have always been commission free both in Vanguard and some in fidelity. Now that you say their own MFs are free in respective brokerages, I may look in to them for my solo 401k in fidelity.

Oh, I wasn’t aware of extra tax paperwork between MFs and ETFs (both formats pay dividends/interest and could pay ST/LT cap gains). I don’t blame you for choosing one if it’s easier though.

I trade so little that $8 for a trade just isn’t that much to pay since there aren’t any annual account maintenance fees. Add to that the number of ETFs that trade free at Fidelity and my total brokerage fees for the year are typically $8-24 I’d say.

Hello RoG,

I hope you can help me with this dilemma…have a taxable account with a lot of Fidelity (free) ETFs. Nothing leveraged or inverse. Just plain and simple ones. The portfolio is up 14% now. I don’t need the cash now. Being a self employed individual I am in a lower tax bracket. All ETFs have been held over one year. Should I sell all (keep gains) and wait for market to crash or should I just leave it alone and add to the portfolio if there is a crash. I don’t want to let go of this gain. Can you advise if the strategy of buying and holding for next 20+ years is better than selling and making profit now and accumulating all over again.

Thanks in advance for your help!

Timing the market correctly is nearly impossible. You have to sell at the right time AND buy back in at the right time. I’d advise your latter approach – keep your $ fully invested and add more periodically over time (especially when it dips!).

Over 20 year periods, the stock market typically does very well (very few, perhaps zero 20 year periods where it’s negative returns though you might want to fact check me on that 🙂 ).

Thank you! Thank you so much!

Hello Justin

Thank you! Thank you so much!

You all have a great trip to Europe-Enjoy!

Hey where do I find your current portfolio fund selection, including-Dividend focused portfolios/REIT ETC.

Much appreciated

Steve

Best place is probably a table in my latest article on dividends.

I’m one of those people that find stocks very abstract and daunting, so most of my investment is in target retirement funds from vanguard and real estate. Dividends piqued my attention mostly because of zero taxes if one is in 15% tax bracket,

I would like to understand the relationship between dividend yield and rental yield (cash after deducting all operating expenses), are they comparable?Lets say, I have a property worth 1M that yields 40K annually (net after all expenses), is that a better investment than cashing out and putting into dividends?

Not sure if you can evaluate $1M of real estate with $1M of dividend paying stocks/funds since the $1M could be a great real estate investment (with a high yield, high prospects for appreciation, for example). Real estate also comes with more risks (leverage, geographic concentration) than dividend stocks/funds (often nationally or globally diversified across industries and economies). So all else being equal, I would require more yield from a real estate investment than from a dividend fund to offset that risk.

I think that depends on your needs and tax situation too. If you need to use the $40k, then your returns from your property can be easily withdrawn, and you get whatever tax benefits from owning your real estate.

If you don’t really need to use the money, your dividends can be reinvested in a DRIP, and you don’t have to worry about what to do with it. Additionally, the capital gains tax bracket is often lower for most people.

Thanks Justin and Smart Money MD!

Good point about DRIP, I was mostly thinking about early retirement from the 40K rental income which would suffice for my living expenses..but the fact that the 1mil is not liquid bothers me so maybe dividend stocks is the way to go. However, I’m guessing the yield I can expect from dividend stock will be around 2.5-3% so around 25-30K a year?

Is there just 1 single vanguard dividend stock I can buy and not monitor continuously? Strangely, I find real estate so much easier as I don’t have to think about it or rebalance anything constantly ????

Thanks Justin and Smart Money MD!

Good point about DRIP, I was mostly thinking about early retirement from the 40K rental income which would suffice for my living expenses..but the fact that the 1mil is not liquid bothers me so maybe dividend stocks is the way to go. However, I’m guessing the yield I can expect from dividend stock will be around 2.5-3% so around 25-30K a year?

Is there just 1 single vanguard dividend stock I can buy and not monitor continuously? Strangely, I find real estate so much easier as I don’t have to think about it or rebalance anything constantly 🙂

Vanguard actually does: VHDYX is the index fund, and VYM is the ETF. I don’t personally own them, simply because I have just been contributing to the total stock market fund, but I guess a dividend index isn’t a bad idea. I believe there is about a 3% annual yield.

It really goes to show you that you can build nice cash flow and attractive yields from by using funds/ETFs. I still like some individual stocks to drive yield a little higher in my portfolio, but as you say, Motif is a great way you do this as well.

I like the lazy approach 🙂 I’d probably go through Motif to “roll my own” dividend stocks strategy if that was the way I wanted to go though. Looks pretty simple.

Thanks for sharing the asset allocation of your portfolio. It’s very helpful and interesting to see how you’ve sliced your portfolio (versus VTSAX/bond split like JLCollins). I have two questions:

1) You hold up to 3 different funds for a single asset class (ex: VSIAX, VBR, IJS for US small cap value // VTMSX, VSMAX, FSEVX for US small cap // etc). Could you share the reasoning behind this?

2) are the asset allocations the same or have they changed since you posted this a year ago?

Thank you!

Sara

1. Different funds due to different options available where specific accounts are held. Some $ is at Fidelity, some at Vanguard. Some in 401ks with access to limited funds.

2. Asset allocation is same as last year. Haven’t tweaked the asset allocation since 2008 or so when I moved to a more aggressive asset allocation with small cap international, international REIT.

I have about 300k in high dividend REITS (NRZ, NLY, AGNC etc.) at the moment generating just over 30k in dividend income a year. The portfolio has appreciated to around 350k in the past 4 years or so and generated another 100k in dividends. I’m not FIRE yet but merely just backtesting my strategy and so far it’s worked out pretty well. I reckon once I have 750k in my brokerage account, I will diversify the portfolio a bit more and give the early retirement a shot. Will likely have 300k in the 401k by that point, and rental income from my Manhattan apartment (about 5-10k a year). Hoping to accomplish this by 35.

What are people’s thoughts on retiring and living off a high yielding REIT portfolio? Crazy? Uncalculated?

I reckon I’ll only need about 20-25k a year where I’m going, perhaps 30k since REIT dividends are taxed as regular income. I’ll be doing things that generate income as well (dive instructor/dive photographer, blogger etc.).

The strategy could work, as long as you’re committed to living off just the dividends. I imagine those REITs are more volatile in terms of share price and dividend stream versus lower yield, more conservative REITs.

Some companies are good at consistently earning money but still don’t pay any dividends at all. Warren Buffett’s Berkshire Hathaway is one of those companies.

Oh yes, so true. And if you look at a graph of the growth, there is a only a slight bump that lasted 2 years and its right back up there. I am slowly getting an idea about how to stay the course in Equity’s.

My BRK-B is up 200%, and still going, I don’t intend to ever sell it.

I love Berkshire Hathaway and Warren Buffett. I don’t own any of the stock other than through index funds but really respect Buffett as an investor and manager.

Hi! I am a new reader and very encouraged by what you have done!

Is there any specific reasons for owning different funds/etf in each sector? Wouldn’t it be more cost effective and easier to track if we just own one fund for each sector?

Also, how did you decide these different sectors? I am still trying to figure out funds/ETF. Most ppl seems to just own Vanguard Total Stock Market Index.

Thank you!

I had accounts at several places like Vanguard, Fidelity, 401ks with different investment options, etc. Some places offered free ETF trades of certain kinds so I ended up picking from their free list. End result: several different funds in same asset class. Not intentional, just what happened to economize.

For asset allocation, I followed a guide I found 10 years ago and established the asset allocation at that point, and stuck with it since then.

I just started dividend investing this year. I find it comforting to know that every month I should receive a payment for doing almost nothing.

My hope some day is to retire early on my dividend portfolio and live off that until I can access my TSP and iRA.

Sounds like a good plan! And I agree – I love sitting back, doing very little and watching the cash roll in on a routine basis. Must be how kings and queens felt back in the middle ages. 🙂

Hi Justin,

Have been an ardent reader of your posts but first time commenting or the better way to put it, writing to ask you a question. The asset allocation you have is 50% US / 50% International. That makes sense to me and I am trying to go down that path as well.

But one thing that is keeping me from allocating so much of my portfolio to international stocks is the fact that some countries tax dividends at the source. And we don’t have a way to recoup that especially when those investments are in tax-deferred and/or tax-free accounts. How do you reconcile with that? Or am I missing something?

Here is a link I found but there are several that discusses the same issue.

https://www.thebalance.com/potential-pitfalls-of-global-investing-through-a-roth-ira-358032

Your feedback is much appreciated.

Best.

I didn’t see a huge downside mentioned in the article, at least not one specific to IRA vs taxable accounts. The main negative of holding International in IRA is the withholding of taxes overseas and you can’t get it back (as you mention). In taxable accounts, you can take the foreign tax credit. I decided to slightly tilt my taxable accounts to have more international investments so I could take advantage of the foreign tax credit. It’s usually a few hundred dollars per year on a $300-400k account balance. The downside to this approach is that international funds tend to pay out a slightly higher dividend yield in my experience, which leads to higher taxes (or at least higher AGI), especially considering international investments often don’t pay 100% of dividends as qualified dividends (unlike the typical large cap US index fund).

So there are pros and cons to sticking international in taxable vs tax deferred, but the dollar amount of tax difference is usually rather modest.

This is coming pretty late, but what are your views on VYM now – still good?

Good as ever I suspect. Expense ratio still nice and low!

Sorry, but you suggest that we can use your dividend ETFs/stocks, but I didn’t see any? Can you please suggest where to find them? Also, do you receive the entire dividend or you reinvest it?

Your portfolio resembles Paul Merriman’s Ultimate buy and hold portfolio. I’ve been thinking about using that portfolio in retirement as well.

I copied the main structure from the Merriman model portfolio!

Any updates on current holdings?

Pretty much the same allocation at this article, except I have 90% in equities and the other 10% in bonds now (bond fund VBTLX or ETF version, BND). This will probably be my asset allocation for the next 4-5 decades.

Question on the dividends paid inside tax deferred accounts: could you have those dividends deposited in your bank account quarterly? Or you have to automatically reinvest them just because they are in tax deferred accounts? Thanks!

From my understanding dividends earned in tax deferred accounts (401K, etc) are subject to the same withdraw rules. So, technically you could have it deposited directly to your bank account, but you would be subject to the 10% penalty in addition to paying taxes on it.

In general, no, you would not want to withdraw them quarterly unless it’s a qualified penalty free withdrawal. Such as if you are pulling from a Roth account or from a 457 account.

In my case, I reinvest the dividends in tax-deferred accounts because I don’t need the extra income today and I prefer to keep as much as possible in the Roth accounts for long-term tax free growth.