Hello and welcome back to Root of Good! The month of May just wrapped up which means it is time for another update. The biggest news is our middle child finished high school a year early! She wrapped up her one AP exam and the last days of class during May, and the graduation ceremony is in a few days.

In other exciting news, we are merely days away from hopping on a plane for our two month summer vacation in Argentina and Brazil. Essentially all of the flight and lodging bookings are done at this point. Right now, we are looking closer at what sightseeing we will do while in South America.

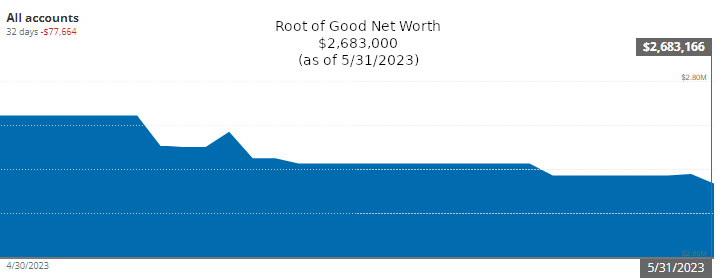

May was a bit of a rough month for our finances. Our net worth dropped by $78,000 to end May at $2,683,000. Our income totaled $1,576, while our spending was $2,976 for the month of May.

Let’s jump into the details from last month.

Income

Investment income totaled $212 in May. Our equity index funds and ETFs pay dividends quarterly at the end of March, June, September, and December. As a result, we had a small amount of investment income last month. Here’s more on our dividend investments.

Blog income totaled $548 for the month. This is slightly lower than my normal blog income.

My early retirement lifestyle consulting income (“consulting”) was $524 in May. That amount represents three hours of consulting last month. That’s a nice slow pace for me to not be overscheduled during the week.

Tradeline sales income totaled $200 in May. Overall, my tradeline income has slowed down in recent months. I get one or two sales per month these days. I ramped up my tradeline sales in 2020 and discussed it in a bit more detail in my October 2020 monthly post and in my July 2021 monthly post.

For May, my “deposit income” totaled $90. This comes from cash back and incentive bonuses from the Rakuten.com and Mrrebates.com online shopping portals (some of which was earned from you readers signing up through these links).

If you sign up for Rakuten through this link and make a qualifying $25 purchase through Rakuten, you’ll get a $10 sign up bonus.

I didn’t get any Youtube income in May. Youtube only pays out when you exceed $100 in accumulated revenue. Recently, my Youtube earnings have been just under $100 per month on average, so I only get paid every other month.

Here is the Youtube channel for the curious. It’s random travel videos, birds, kids, and a couple of DIY videos. There are only a few main videos that bring in most of the traffic (and revenue!).

If you’re interested in tracking your income and expenses like I do, then check out Empower Personal Dashboard, formerly known as Personal Capital (it’s free!). All of our savings and spending accounts (including checking, money market, and five credit cards) are all linked and updated in real time through Empower Personal Dashboard. We have accounts all over the place, and Empower Personal Dashboard makes it really easy to check on everything at one time.

Empower Personal Dashboard is also a solid tool for investment management. Keeping track of our entire investment portfolio takes two clicks. If you haven’t signed up for the free Empower Personal Dashboard service, check it out today (review here).

Tracking spending was one of the critical steps I took that allowed me to retire at 33. And it’s now easier than ever with Empower Personal Dashboard.

Expenses

Now let’s take a look at May expenses:

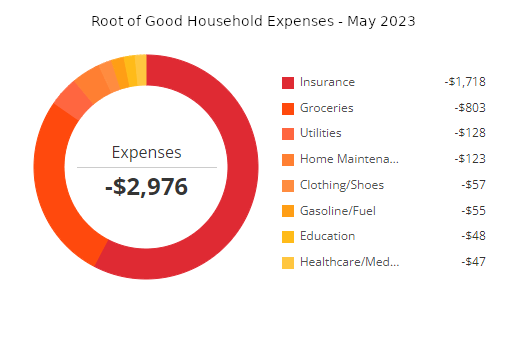

In total, we spent $2,976 during May which is just under our regularly budgeted $3,333 per month (or $40,000 per year). Insurance and groceries were the two highest categories of spending in May.

Detailed breakdown of spending:

Insurance – $1,718:

Our annual home insurance bill and our six month auto insurance bill came due in May. Inflation really hit these two bills hard this year. Our homeowner’s policy climbed 29% to $978 for one year.

The auto insurance bill didn’t suffer such a high percentage increase, however it is higher than we are used to since we added our teenager to the policy. The six month premium for three drivers is $740.

I don’t have a lot of perspective on whether our insurance costs a little or a lot, but I’ve heard of people paying many multiples of what we pay. I guess I cannot complain too much!

Groceries – $803:

Down slightly from last month but still another expensive month of groceries, at $803. Food inflation bumped up our baseline grocery spending. However, I am happy to report that prices continue to flatline and even decline in some aisles in the grocery store.

I saw eggs for $1 per dozen at Aldo so I bought a 10-pack since they were 80% cheaper than 5 months ago. Eggs taste a lot better when they are almost free instead of priced as high as luxury goods like beef.

Utilities – $128:

We spent $8 on our water/sewer/trash bill because I used up some prepaid Visa gift cards that I got from some rewards programs to pay the other ~$100 of the bill.

The electricity charges totaled $80 for last month.

The natural gas bill, which provides heating and hot water, totaled $41 for last month.

Home Maintenance – $123:

$119 for a new garbage disposal. After some brief troubleshooting, I decided the old garbage disposal was dead. It appears the cutting/grinding blades inside of the unit were made of galvanized steel. The inside was severely rusted and seized up from 8 years of use. The galvanized steel was a strange choice of material for something that stays wet for most of its life, given how it can rust.

I decided to upgrade to a better model of garbage disposal when I replaced it this time around. I paid about 50% extra for a more powerful unit (the Insinkerator Badger 15ss 3/4 hp model) that includes an all stainless steel grinding apparatus. Hopefully we’ll get more than 8 years of usage out of the new garbage disposal.

The other $4 home maintenance expense was for a gallon of gas for our lawnmower.

Clothing/Shoes – $57:

Some dress clothes for kid #2’s high school graduation and public speaking class in college.

Gas – $55:

With our oldest teenager driving to college or work on an almost daily basis, we end up buying about one tank of gas each month now. Since we’ll be gone over the summer, and our daughter’s college classes during the summer session are all online, gas expenditures may drop in the coming months.

Education – $48:

$13 for a required t-shirt for kid #3’s elementary school graduation ceremony.

The other $35 of education dollars went toward a college e-textbook. We got lucky for the summer semester, as the textbooks were free for all the other four classes that our two college students are taking. Later in 2023, I will reimburse myself the $35 for the textbook purchase using our 529 account.

Healthcare/Medical/Dental – $47:

Our current 2023 health insurance costs $18 per month, thanks to very generous Affordable Care Act subsidies that we receive due to our low ~$45,000 per year Adjusted Gross Income.

We signed up for 2023 dental insurance plans and paid a total of $29 in premiums during last month.

I chose a very basic plan for $9 per month for me that covers most preventive care but no fillings. Mrs. Root of Good has a different set of dental needs than I do so we kept the more comprehensive $20 per month plan for her (same as 2022’s plan).

By buying insurance, we should save a couple hundred dollars on my dental care. For Mrs. Root of Good, we will still save a few dollars compared to paying cash for the preventive dentist visits throughout the year.

Travel – $0:

No travel spending in May!! We had already booked all the flights and lodging for two months in South America in previous months.

However, there may be some extra travel spending during June to replace a flight we booked. Flybondi, a discount carrier in Argentina, rescheduled one of my flights by 3.5 hours earlier than originally scheduled. This means our 4.5 hour layover turns into a 1 hour layover. Since we have to pick up our checked luggage and recheck it for the 2nd flight, it’s unlikely we’ll make the 2nd flight (with the schedule change). So I am investigating back up flights, and will probably have to charge back the Flybondi flight as they refuse to reschedule the flight for the next day for free (“changes of 4+ hours results in a free change/cancellation”).

In any event, if this is the worst travel snafu we have all summer and I end up eating the full price of these tickets we cannot use, then I won’t worry too much about a few extra dollars on a replacement flight.

If you are interested in getting free travel from your credit card like I do, consider the Chase Ink Unlimited or Chase Ink Cash business cards (my referral link). Right now the Chase Ink business cards offer 75,000 Chase Ultimate Rewards points that can be redeemed instantly for $750 in cash. Mrs. Root of Good and I each received our new Chase Ink Unlimited cards during December, and we just picked up a new Chase Ink Cash card during March. The bonuses keep on rolling in the door!

Chase is pretty liberal when it comes to “what is a business”. If you sell stuff on eBay or Craigslist or do some odd jobs occasionally then you have a business and could get a credit card as a “sole proprietor”.

Another favorite travel card in my wallet is the Capital One Venture X card. The Venture X card is a “keeper” for me. First off, it comes with a $750 sign up bonus after spending $4,000 in the first three months. The bonus is paid in the form of 75,000 bonus points that you can redeem against any travel purchases from anywhere. Then you earn a solid 2 points per dollar spent forever! The other big perk is airport lounge access. You can get yourself plus unlimited guests into Priority Pass lounges. And you plus two guests can get into Plaza Premium network lounges and Capital One Lounges.

The Capital One Venture X card does have one catch – a $395 annual fee. But they reward you every year with an easy to use $300 travel credit plus $100 worth of points. Together, that makes $400 they give you annually which more than offsets the annual fee. Another benefit worth mentioning: you can add up to four authorized users for free, and they also get all the benefits of the Venture X card including the valuable airport lounge access. We used this perk to “gift” a pair of Venture X cards with airport lounge access to my brother in law and his wife to use on their family trip back home to Cambodia in April with their two young children.

Since the annual fee is offset in full by travel credits each year, I personally plan on keeping the Venture X card forever since the card benefits are so great.

Cable/Satellite/Internet – $0:

We generally pay $18 per month for a local reduced rate package due to having a lower income and having kids. 30 mbit/s download, 4 mbit/s upload. Right now the cost of the internet service is temporarily reduced to $0 due to the “Affordable Connectivity Program”.

Year to Date Spending – 2023

We spent $11,317 during the first five months of 2023. This annual spending is about $5,000 less than the $16,667 we budgeted for five months of spending in our $40,000 annual early retirement budget.

The Fall 2023 financial aid packages for our two kids are not yet finalized. However, college costs for our two kids in college should be covered in full by grants and scholarships throughout the remainder of 2023. And we have ample 529 funds should we need to cover anything out of pocket.

The one large expense anticipated for 2023 will be a used car. We failed in our attempts to acquire one during 2022 but that’s okay. The market appears to be cooling off a bit, since I am finally seeing a few cars under $10,000 that aren’t complete pieces of junk. The tentative plan is to buy a second car when we return from South America in August.

Fortunately, we are underspending our budget by a significant margin, so we should be able to “absorb” the used car purchase in our regular $40,000 per year budget without exceeding the budget by much.

Monthly Expense Summary for 2023:

- January – $3,423

- February – $1,675

- March – $1,679

- April – $1,566

- May – $2,976

Summary of annual spending from all ten years of early retirement:

- 2014 – $34,352

- 2015 – $23,802

- 2016 – $38,991

- 2017 – $31,708

- 2018 – $29,058

- 2019 – $25,630

- 2020 – $28,466

- 2021 – $31,740

- 2022 – $29,449

- 2023 – $11,317 (Year to Date through May 31, 2023)

Net Worth: $2,683,000 (-$78,000)

Our net worth slowly declined during May to end the month $78,000 lower than where we started. Our net worth finished the month at $2,683,000. Fortunately, the first week of June has been rather kind to our portfolio with several strongly positive days in the stock market. So we might make up the decline in May throughout the rest of June.

These “small” monthly changes in net worth are fairly routine and represent just a few percentage points of monthly swings. No worries over here! Our spending remains in-line with our budget and portfolio gains continue to keep up with inflation over the past several years. More importantly, we are able to travel when/where we want and enjoy life without worrying about money, which is the most important thing.

For the curious, our net worth reported above includes our home value (which is fully paid off). However, please note that I don’t consider my home value as part of my portfolio for “4% rule” calculation purposes. I realize folks ask me about that every month so I just wanted to state that here for clarity.

Life update

Things are going swimmingly for us. We have a big two month trip coming up in just a few days’ time.

It will be winter in South America when we arrive, so we are mentally trying to prepare for colder weather (mostly in the 60’s during the day but it can get chilly at night). Fortunately it hasn’t been too hot yet in North Carolina so it won’t be too much of an adaptation.

I am interested to see how the kids enjoy the mild winter weather instead of our normal summer weather at home and abroad in our typical vacation destinations. It’s our first time heading south of the equator for our big summer vacation. I think it will be much nicer to be too cold instead of too hot. We can always bundle up and find warmth inside a building somewhere. However, in summertime, it can be a challenge to find functioning air conditioning during hot weather in places outside of the USA.

In preparation for the six weeks we’ll spend in Argentina, a Spanish speaking country, our 11 year old son has been practicing Spanish on Duo Lingo. He’s on a 45-day consecutive streak right now and really enjoys challenging himself and leveling up his Spanish to catch up with the rest of the Spanish speakers in our household. Hopefully he gets to practice his Spanish while we are down south! Quisiera dos empanadas, por favor.

In addition to prepping for our summer trip during May, I also spent some time with a bunch of FIRE friends at CampFI Midatlantic. I declined to speak at the 2023 camp, thinking I might have other travel plans booked during May that would conflict. But at the last minute, I got a call from the camp organizer, Stephen Baughier, inviting me up there for the four day, three night camp that takes place at a summer camp on the James River in Southeastern Virginia. I didn’t have to speak this year, but I did volunteer to moderate a breakout session on travel hacking and credit card rewards to “earn my keep”.

It was great catching up with some old friends that have been to CampFI before, as well as make new friends in attendance for the first time! After an exhausting but fun weekend, I was ready to get back to my normal peaceful life in Raleigh. It took a couple of days for my vocal cords to recover after chatting so much over the long weekend at CampFI.

If you are interested in attending a CampFI event at any of the six locations throughout the USA, the cost is about $300-450 for three nights lodging, three meals a day, plus presentations from four FIRE-oriented speakers. But the real appeal comes from being surrounded by 70 to 80 smart people who are generally interested in some version of financial independence.

I snagged a 10% discount code that is supposed to be for past CampFI attendees only, but I got special permission to share it here (because I love a discount as much as anyone). Promo code “CFMA2023” is valid through June 30, 2023 and will give you 10% off any upcoming CampFI (you can book tickets at campfi.org ).

I make nothing if you buy tickets with that code, and CampFI doesn’t pay me a penny (other than comping me a ticket when I speak at a camp). I just think it’s a well-run program and a good value given the cost if you are interested in FIRE and want to learn more or meet others on the same life path.

Ok folks, that’s it for me this month. Tune back in next month when I’ll be reporting live from beautiful Buenos Aires, Argentina!

Got anything going on or any big trips planned in the next couple of months?

Want to get the latest posts from Root of Good? Make sure to subscribe on Facebook, Twitter, or by email (in the box at the top of the page) or RSS feed reader.

Root of Good Recommends:

- Personal Capital* - It's the best FREE way to track your spending, income, and entire investment portfolio all in one place. Did I mention it's FREE?

- Interactive Brokers $1,000 bonus* - Get a $1,000 bonus when you transfer $100,000 to Interactive Brokers zero fee brokerage account. For transfers under $100,000 get 1% bonus on whatever you transfer

- $750+ bonus with a new business credit card from Chase* - We score $10,000 worth of free travel every year from credit card sign up bonuses. Get your free travel, too.

- Use a shopping portal like Ebates* and save more on everything you buy online. Get a $10 bonus* when you sign up now.

- Google Fi* - Use the link and save $20 on unlimited calls and texts for US cell service plus 200+ countries of free international coverage. Only $20 per month plus $10 per GB data.

Graduating high school one year early is impressive! What was her motivation and where is she going to college, if she’s going?

Was there a particular grade that she skipped? I could’ve graduated with you earlier, but I was held back I think in kindergarten or the first grade to just match my peers.

Enjoy Argentina!

Sam

She has one more year of community college (she did 1st year during high school), then she hopes to transfer to NC State University for a degree in Comp Sci.

No particular grade that she skipped. She had enough HS credits to graduate early, and only had to take a 2nd English class this year (her 11th grade year) to graduate a year early (we need 4 English credits in North Carolina to graduate HS).

Cool beans. That means college will be very inexpensive!

What about transferring UNC Chapell Hill? Seems to be a well/regarded program and still in state tuition.

Sam

It’s a possibility, but I think they accept less in the form of transfer credits/AP scores. So it might add another 1-2 semesters of study. Haven’t looked closely though.

My mom did something similar — she accelerated her courseload to get the heck OUT of rural Indiana a year early and go to college in DC in the late ’60s. That ended up working out pretty well. Congratulations and well done to your daughter!

Nice! So much opportunity out there.

I graduated a year early from HS as well! I was so done at the time, but looking back I miss having half days and what “senioritis” look like. However, it allowed me to have a break year after college which was one of the best year’s ever. Nice back patio you go there. Is a pool a luxury out there?

Pools aren’t exactly a luxury, but in my older neighborhood, I’d say maybe 10% of the homes have pools? Our house used to have a pool before we bought it but (fortunately) they filled it in. I don’t think I’d use it that much. And the cleaning/servicing would be a pain in the butt. However, sitting out on the back porch is really really nice!

Justin – very important question: What are you going to do with 10 dozen eggs mere days before a two-month trip??? :-}

We bought them a while ago, just now sharing the pics 🙂 With 5 of us, we can eat a few dozen a week without really trying. Also do some baking from time to time.

Like Sam, I’m curious about graduating from high school a year early. I had been thinking dual-enrollment instead though. I didn’t know you can push through high school earlier.

Congrats on getting on the Duolingo bandwagon. I was interested in learning Japanese, so I picked up it nearly 5 years ago. I had my kids pick it up too. None of us are serious about it, just earn the minimum to keep the streak alive. They’ve bounced between a half-dozen languages of their choice. They never do Spanish or French that they’ve already had in school. I drift from Japanese back to Spanish quite a lot. Overall, we would be very bad in any place were we’d need to speak the language, but I think there’s a good foundation. At 9 and 10 that’s all I’m looking for. They can focus more on something like your kid does when the actual trip comes up.

I would be interested in CampFi. They never seem to come close to New England though.

I responded to Sam upthread re: graduating early too.

Both the older 2 kids also did dual enrollment HS/community college their 11th grade years before graduating early. So they managed to get about a year of community college done by the time 11th grade was over. Lots of educational opportunities here for our high schoolers. As a result, college will be almost free (they get paid several thousand dollars when in community college; 4 year university might cost a couple thousand dollars net each year but they only need 1.5-2 years of 4 yr university).

Re: Duolingo – it’s going pretty well for our 11 year old. I am SHOCKED that he’s pronouncing things correctly and knows a lot of words, but we also speak Spanish at home a lot and many of his classmates speak Spanish natively. So maybe that’s helping too? I am really hoping he gets to extend that learning and apply some of it during the first 75% of our trip this summer when we’re in Argentina (six weeks)

Oh my hope you love Brazil as much as we did ! It depends where you’ll go of course. Brazil is larger than the continental US but most people don’t realize that. My best friends are brazilians and they are amazing, always receiving tourists with open arms. Argentinians not so much but I had no problems there as well.

Iguazu Falls is the big attraction and I am sure we will find it amazing. Sao Paulo is our other stop in Brazil, for 1 week. Of the 4 places we are visiting I am least excited about it. But figured “big city Brazil, let’s do it 1x in our lives!” so we’re going ha ha 🙂 This was partly a “free” layover to get our flight schedule home to work out better without a ridiculously crappy set of layovers coming from Iguazu Falls to Raleigh. So we stop in Sao Paulo on the way home for a week and enjoy the city and food, then have a super easy connection in Miami on the flight home.

Thanks for the update I always like reading them. , where you have a portion of your NW In retirement accounts, I guess you don’t have access to those or the dividends? And basically spend from the accts you are allowed access to?

Do you have your allowable divs paid direct to your checking acc plus your income/s and that is how you cover your life and day to day expenses? I just wondered how you pay for your day to day life as I don’t think you’ve reported that?

Have a lovely holiday!

Yes – we do not need to withdraw dividends from our retirement accounts. But I do include those in our total dividend income because we theoretically could pull out most of those retirement acct dividends through various means.

And yes to your 2nd question – I transfer the dividends over to my checking account soon after they get paid and then I spend them 🙂 These are mostly quarterly dividends and it covers 1-2 months living expenses each quarter (on average). Other income comes from this blog, my consulting, tradeline sales, some bonuses from credit cards and brokerage account sign ups, and anywhere I can find a free buck!

Thank you so much for your reply, really helpful

I look forward to hearing about your big trip

Kind regards

Thank you for your monthly update! Reading your blog I have the impression you are 100% invested in stocks with no bond allocation, has that changed after retirement? If so, to what percentage? My wife and I are aggressively investing to reach FIRE (she is 37 I am 44) and are 100% stocks for now. We plan to allocate 20% to bonds once we reach our FI number. Thank you!

I am at 90% stocks since about 2017. Holding steady there since I am okay with a lot of equities risk!

Regarding the used car… I don’t know if you’re set on $10k and under. But if you’re willing to increase the budget a bit, the “cheapest NEW car” that you can buy in America right now is a 2023 Nissan Versa for $16k. It’s new so obviously won’t be junk and will definitely last a long time.

I priced one out and it was $23000 by the time I was done with it. I’d take a new $16k Versa if it was automatic but couldn’t find one.